Aside from a home, higher education may be the most expensive and most important purchase in a person’s lifetime.

Chinese philosopher Lao-Tzu said, “Even a journey of a thousand miles begins with a single step.” And that’s probably where you are now — looking to take that first step in planning for your loved one’s future education expenses. In this section, we invite you to learn more about:

Starting Early

Today, the average cost of a four-year undergraduate education is more than $93,680 at a public college and more than $208,040 at a private college.1

That’s a considerable amount for any family to accrue, but if you start saving early, you can potentially take advantage of the power of compounding savings and interest for a longer period of time.

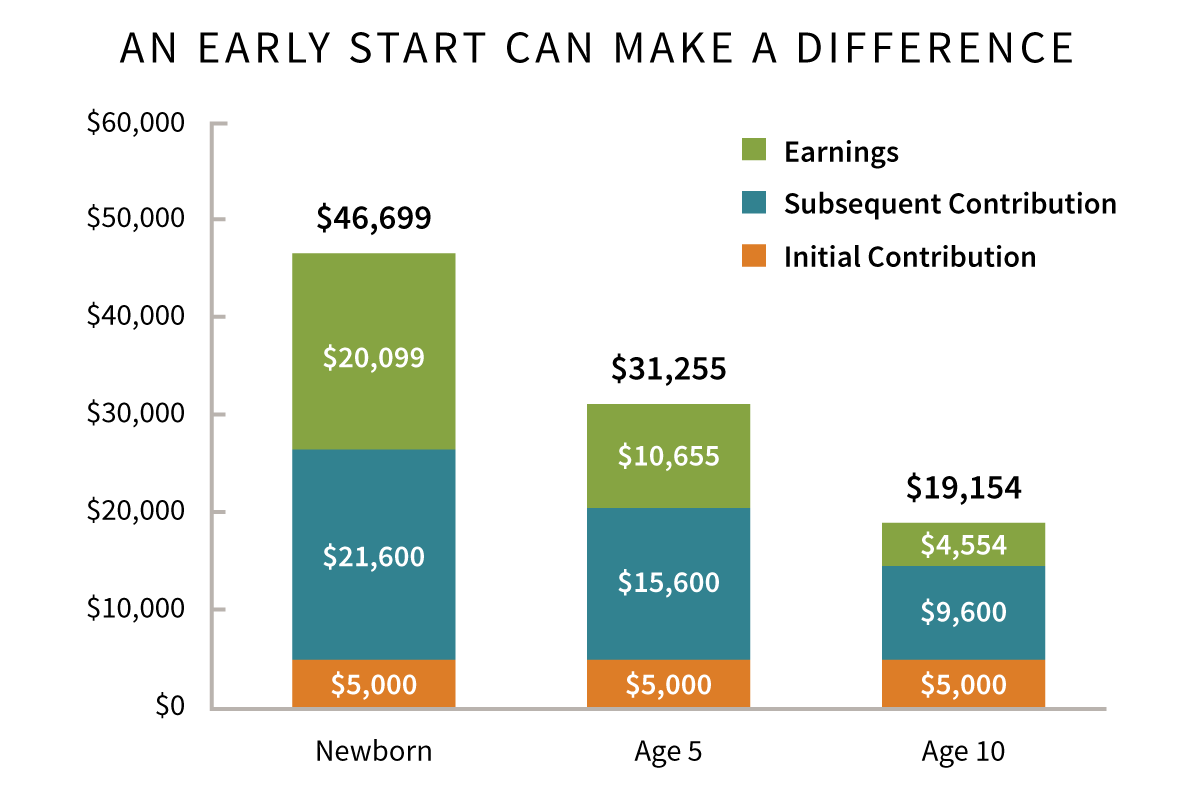

In the chart below, you can see how

529 Plan:

A state-sponsored, tax-advantaged college savings program established under and operated in accordance with IRC §529 to help save for qualified education expenses.

contributions might grow if you start with $5,000 when your child is a newborn and continue saving an additional $100 per month until your child turns 18.

This chart assumes a $5,000 lump sum investment, $100 monthly investments and 5%

Annual Rate of Return:

The rate of return on your investment, expressed as a percentage of the total amount invested.

The calculations are for illustrative purposes only, and the results are not indicative of the performance of any investments. The calculations do not reflect any plan fees or charges that may apply. If such fees or charges were taken into account, returns would have been lower. With any long-term investment, investment returns may vary. Such automatic investment plans do not assure a profit or protect against losses in declining markets. Any earnings are federal tax free if used for qualified education expenses.

1Source The College Board, “Trends in College Pricing and Student Aid 2020”. The average yearly estimated full-time undergraduate budget for tuition and fees, room and board, and books and supplies is $23,420 for in-state public four-year institutions (on campus) and $52,010 for private non-profit four-year institutions (on campus). The estimated costs for both public and private institutions assume the account beneficiary will start college at the age of 18. Please note that this is only an estimate and does not include transportation or other expenses.

Saving Regularly

By choosing to make regular contributions that fit your budget, you can ensure that saving for college becomes a part of your monthly investment strategy. Soon, you may find that saving and investing become a habit, and planning for the future is easier than you thought. You can establish a plan to save regularly by setting up an automatic investment plan1.

Whether your monthly savings budget is $50 or $250, contributing a fixed amount into a 529

Account:

A savings trust account established by an Account Owner pursuant to the Savings Trust Agreement for purposes of investing in one or more portfolios. Accounts are part of the Plan and are held in the name of the Plan on behalf of and for the benefit of the Account Owners and the Beneficiaries.

could really help your savings add up over time.

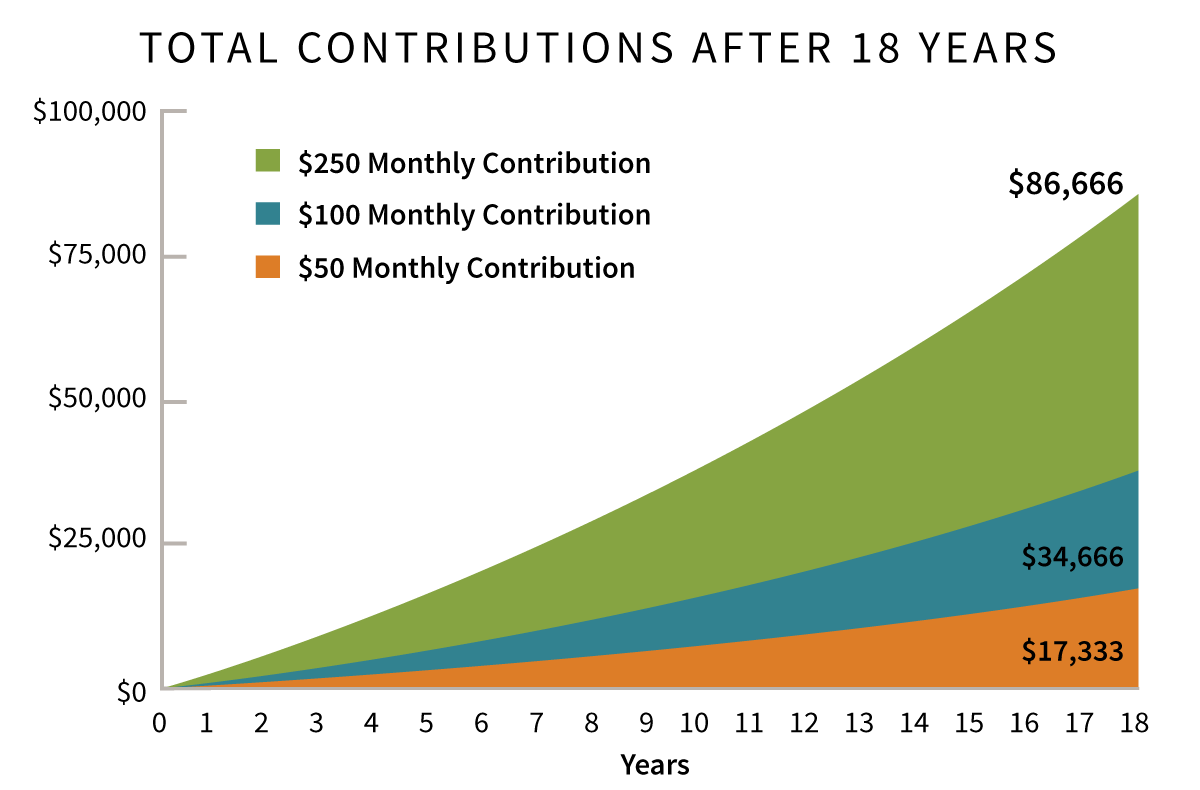

The chart that follows shows how an investment could grow over 18 years, using an automatic investment plan with regular monthly investments of $50, $100 or $250.

This chart assumes a net 5%

Annual Rate of Return:

The rate of return on your investment, expressed as a percentage of the total amount invested.

. The calculations are for illustrative purposes only, and the results are not indicative of the performance of any investments. The calculations do not reflect any plan fees or charges that may apply. If such fees or charges were taken into account, returns would have been lower. With any long-term investment, investment returns may vary. If used for qualified education expenses, any earnings would be federal tax free.

1Automatic investing does not assure a profit and does not protect against loss in declining markets.

Scholarships & Aid

Consider Scholarships and Aid

There are many ways to help close the gap between the cost of college and the funds you have available. First, you’ll need to educate yourself on the many ways to offset the cost of education. Consider the following:

Scholarships: A wide variety of financial scholarships are available to many deserving students.